How to claim the Job Retention Bonus from 15 February 2021

12 October 2020

HMRC has recently published guidance on how to claim the Job Retention Bonus. The £1,000 bonus is available to employers for each eligible employee they furloughed and kept continuously employed until 31 January 2021.

From February 2021, employers will be able to claim the Job Retention Bonus through the gov.uk website. The Job Retention Bonus will be a one-off payment of £1,000 to the employer for every eligible employee that is claimed for. The bonus will be taxable, so the business must include the whole amount as income when calculating their taxable profits for corporation tax or self-assessment.

You’ll be able to claim the bonus between 15 February 2021 and 31 March 2021. You do not have to pay this money to your employee.

Who can claim the Job Retention Bonus?

The bonus is available to all employers who have furloughed employees and made an eligible claim through the Coronavirus Job Retention Scheme (JRS) also known as the furlough scheme.

You can still claim the bonus if you make a claim for any eligible employees through the Job Support Scheme that launches on 1 November 2020.

Eligible employees you can claim for

There are a few eligibility criteria to be aware of, before you start preparing to make your claim.

You can claim for employees that:

- You made an eligible claim for under the JRS

- You kept continuously employed from the end of the claim period of your last JRS claim for them, until 31 January 2021

- You are not serving a contractual or statutory notice period for you on 31 January 2021 (this includes people serving notice of retirement)

- You paid enough of an amount in each relevant tax month and enough to meet the Job Retention Bonus minimum income threshold

It’s worth noting that you can still make a claim for the Job Retention Bonus, even if HMRC is checking your JRS claims, your payment may just be delayed. HMRC will not pay the bonus if you made an incorrect Coronavirus Job Retention Scheme claim and your employee was not eligible for the Coronavirus Job Retention Scheme.

How to prepare for your claim

The bonus will be open for claims from 15 February 2021. In the meantime, it’s worth noting the areas you need to prepare so you can make sure you’re all set when the time comes.

You need to ensure:

- You’re still enrolled for PAYE online.

- You comply with your PAYE obligations to file PAYE accurately and on time under Real Time Information (RTI) reporting for all employees between 6 April 2020 and 5 February 2021.

- You keep your payroll up to date and make sure you report the leaving date for any employees that stop working for you before the end of the pay period that they leave in.

- You use the irregular payment pattern indicator in Real Time Information (RTI) for any employees not being paid regularly.

- You comply with all requests from HMRC to provide any employee data for past Coronavirus Job Retention Scheme claims.

If you outsource your payroll to a payroll team, your appointed payroll provider will be able to make the claim for the Job Retention Bonus on your behalf.

HMRC has advised they’ll update their Job Retention Bonus guidance further at the end of January 2021. In the meantime, it’s a good idea to get started with your record keeping to ensure you have processes in place to capture the data needed, in the lead up to the claim window opening.

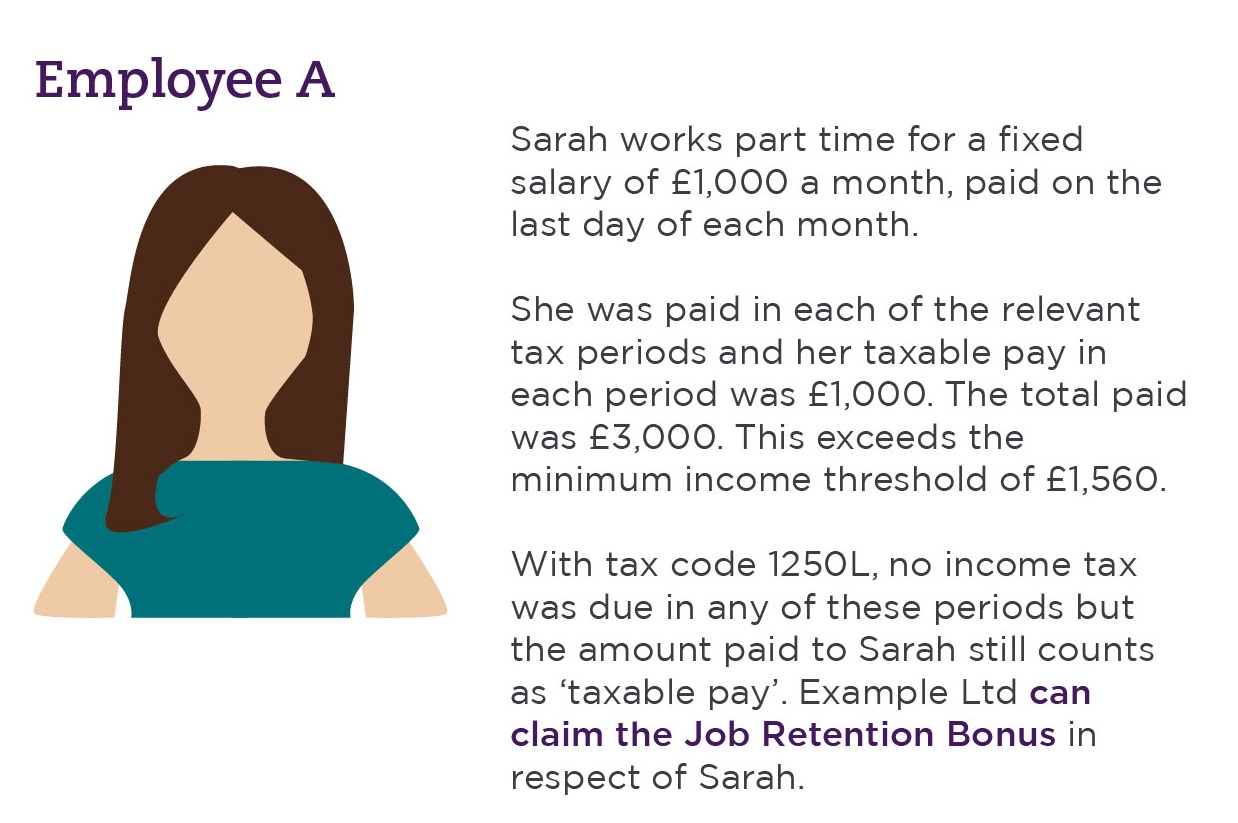

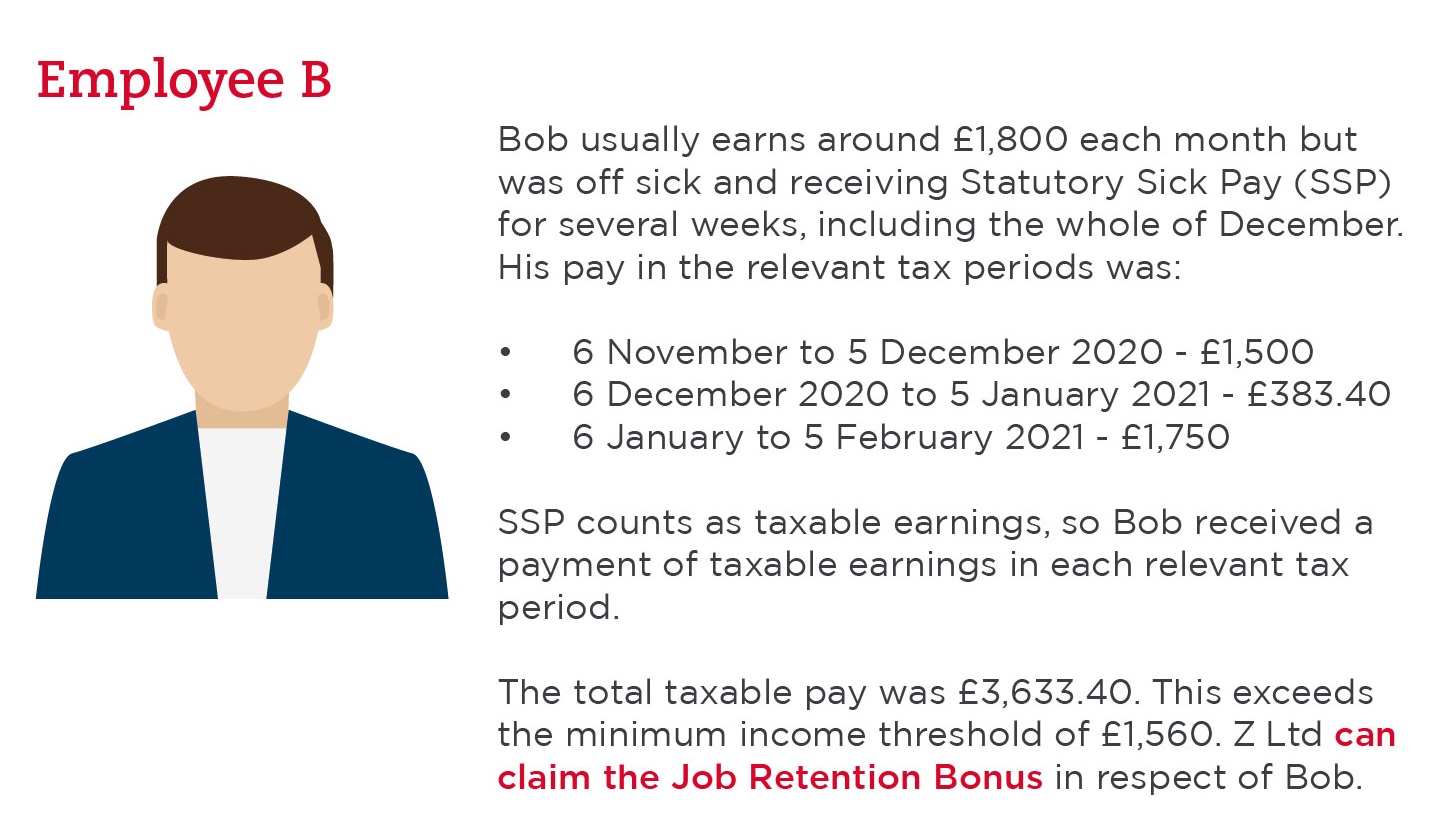

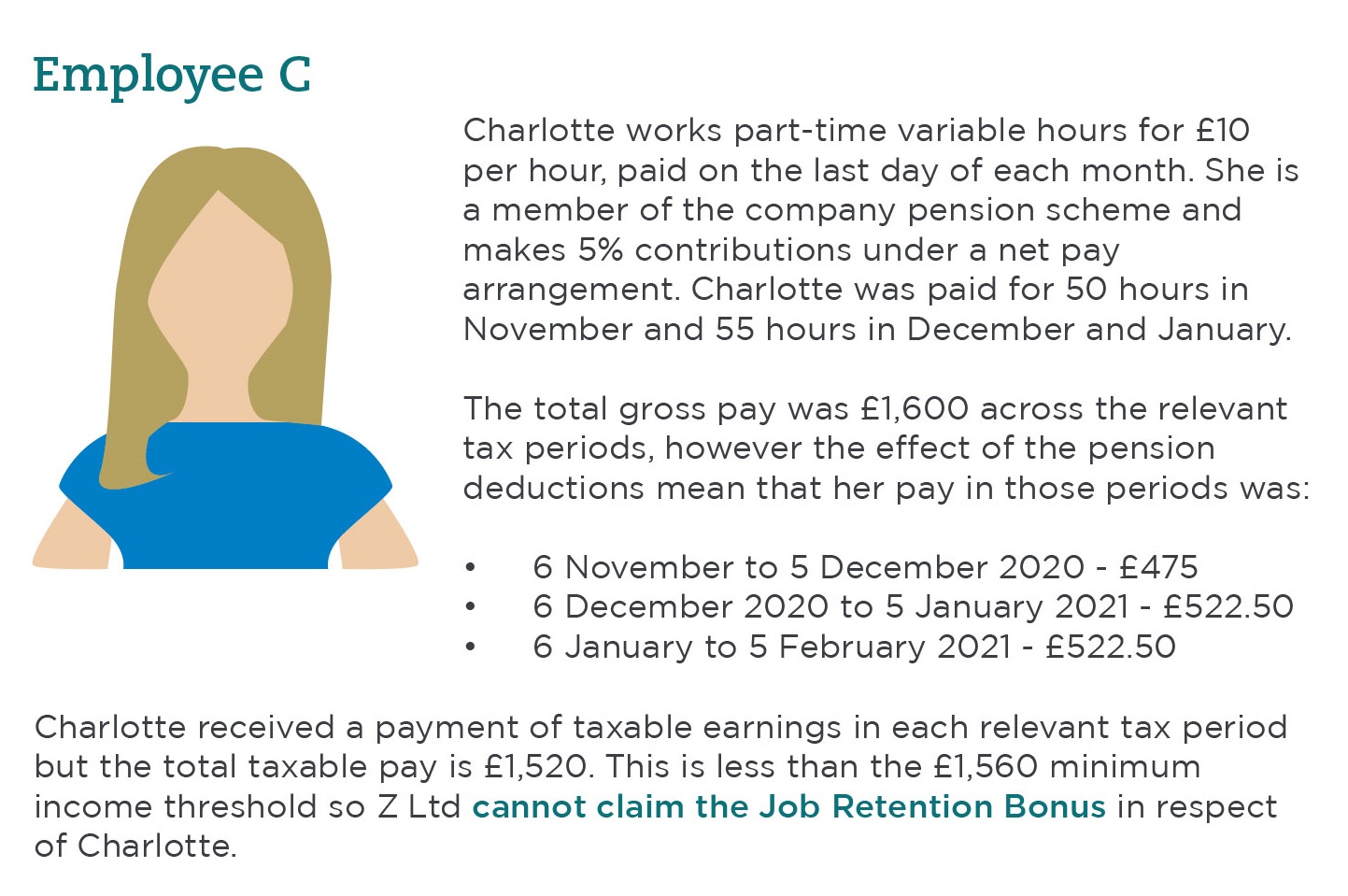

The minimum income threshold

To be eligible for the bonus you must make sure that your employees have been paid at least the minimum income threshold. To meet the minimum income threshold, you must pay your employee a total of at least £1,560 (gross) throughout the tax months:

- 6 November to 5 December 2020

- 6 December 2020 to 5 January 2021

- 6 January to 5 February 2021

You must pay your employee at least one payment of taxable earnings (of any amount) in each of the relevant tax months. The minimum income threshold criteria apply regardless of:

- how often you pay your employees

- any circumstances that may have reduced your employee’s pay in the relevant tax periods, such as being on statutory leave or unpaid leave

HMRC will check that your employees have been paid at least the minimum income threshold by checking information submitted through Full Payment Submissions via Real Time Information (RTI).

Example Calculations – Eligibility

Here to help

If you would like to discuss this further, or find out how Johnston Carmichael can help you at this challenging time, please don't hesitate to get in touch with me or your usual Johnston Carmichael adviser.